Watch Video to Find Out More About Us

The UK's Leading Property Education Provider

What Our Members Say about Property Wealth System

Prepare To Have Your Mind Blown!

Fantastic, comprehensive content delivered by a team of knowledgeable, down to earth experts.

Explanations are concise, considered and detailed with lots of opportunities for discussion and questions. High level, quality information you cannot find anywhere else.

You will learn things that are more valuable than any university degree. Delivered in a supportive, non judgemental environment.

What this team don't know about property, isn't worth knowing. Amazing. Intense. Fun. Mind blowing. Sign up now. You will not regret it!

PWS 3DI Programme

Amazing days at the property investment course in Solihull.

Caroline and her team ooze knowledge, passion and enthusiasm for property investment.

The event provides useful information, in abundance, delivered in such a clear and concise way.

I would encourage anyone who has an interest in property investment to sign up and attend as it will help you prepare your property investment strategy and propel your business forward.

One key takeaway from this course is “knowledge is power”.

Highly Recommended!

Caroline and her team are incredible!

The intensive course was super informative, eye-opening and engaging from start to finish. The training was a mix of direct teaching, case studies, 1:1 consultants and group discussions.

I particularly liked that the course combined property investment strategies with practical, real life (and often live) examples of purchases.

Caroline are her team are very humble and approachable. All in all, an insightful 3-day course and a fantastic start to my property investing journey..

About PWS

The Property Wealth System is a network of active investors who have enjoyed individual success following this system and want you to enjoy the same.

Property education is more than just information, it’s information and action. Action with misinformation is dangerous, information without action is pointless. The Property Wealth System is the perfect blend of real information, personal mentoring and your personal action.

Our Courses

Property Wealth System combine a perfect blend of digital content with bespoke, personalised coaching and training. Our team of seasoned investors are on hand to help you in your property strategy; from buy-to-let through to large scale developments. The PWS team and PWS member network have a wealth of experience and knowledge for you to tap in to.

5 Star Rated

Property Workshop

The Gateway to Investing in Property.

Join Caroline Claydon and the team for the best Property Education Training in the UK. Rated 4.9 on Trustpilot, the Property Wealth System Property Workshop will blow your mind wide open.

Caroline has delivered this training for over 10 years to thousands of investors. Whether you are an aspiring investor or have already begun this course with over 27 hours of training is for you. Check out the reviews on Trustpilot to see what you can expect.

Digital Courses

Our e-learning platform is the most comprehensive, relevant and advanced in the industry. There is nothing like it available elsewhere.

The Property Wealth System has over 100 hours of structured up to date e-learning for you to digest at your pace, over and over again. We have organised it into 10 content packed courses with real-life case studies and examples as well as resource packs. The Property Wealth System is your own property university at your fingertips, whenever you want to learn and wherever you want to learn from!

Personalised Masterclass

Enjoy a personalised and bespoke Masterclass that will create the solid foundation of your property business and build your confidence as a professional property investor. Our Masterclasses are industry-leading and built on the principle of ASK: Accountability, Support, Knowledge. The Masterclasses underpin your Digital Course learnings and provide the bedrock for your property business. You will be allocated into a small group and meet virtually.

One to One Mentorship

The personal one-to-one mentorship is the ‘jewel in the crown’ of our Property Wealth System training. A bespoke 6 month personal mentorship which takes place in YOUR investment area. A buying trip with a property expert plus personalised coaching sessions. The mentorship is designed for those who want to accelerate quickly in their chosen strategy, or those looking to step up to the next level and implement some of the more advanced property strategies; such as HMOs, Developments, Hotels and SA or Commercial Property.

Boot Camps & Specialist Implementor Training

Spend time with a PWS Mentor to implement your strategy in small personal classes. Focused on active learning looking at your area, deals, opportunities and ultimately action plan. An excellent opportunity to network and learn in a practical, current and interactive environment.

Each Implementor training is focused on a strategy for example; HMO, Short Stay, Developments, Commercial & Compliant Sourcing to name a few of them.

Resources & Power team

The PWS Resource Library is packed full of free calculators, deal analysers, trackers, templates, reading lists and systemisation tools. Plus of course a pre qualified little black book of property experts from brokers, accountants, solicitors to capital allowances, designers and more.

Frequently Asked Questions

Common questions answered.

What strategies do your courses cover?

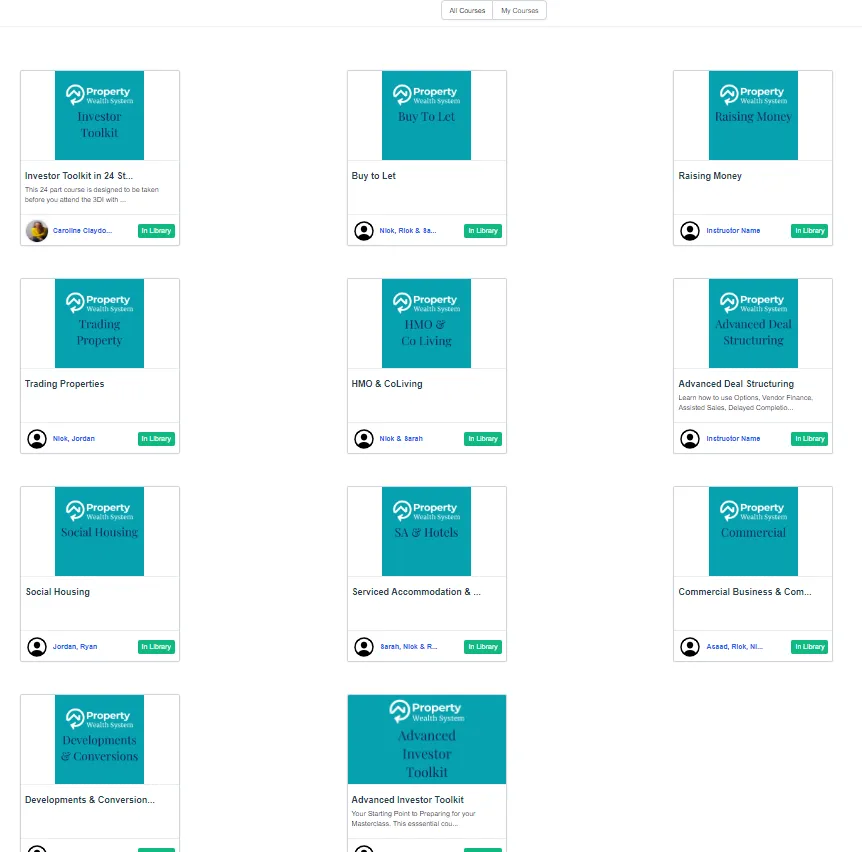

We have 10 Digital Courses of around 10 hours each, with trainer presented modules, case studies and resources. Topics are:

Advanced Investor Toolkit

Buy to Let

Raising Money

Trading Properties

Advanced Deal Structuring

HMO & Co Living

Serviced Accommodation & Hotels

Developments & Conversions

Social Housing

Commercial Property & Business

Do you offer personalised coaching?

Yes. We have a 6 Month Masterclass led by a PWS coach on zoom. The classes are small enough to get personalised guidance and big enough to be able to network. The classes are suitable for beginner to advanced investors and cover real deal analysis, deal structuring and accountability across all property strategies.

What is your one to one mentorship?

We have 13 years experience supporting property investors in the field. What this means is a 6 month programme with a PWS coach that includes up to two full days in your investment area, talking to agents, meeting vendors, viewing properties, analysing properties and ultimately making offers.

You also work with your coach after the in field days to follow up and keep the momentum. This is available for any property strategy and you will be matched with an expert in the strategy you have chosen.

Do you offer strategy specific classroom teaching?

Yes, our Strategy ImpleMENTORS

How do I purchase one of your courses?

Our Online Shop is imminent but in the meantime you can register your interest below.

How many property coaches does PWS have?

PWS coaches have been coaching investors since 2011, we have fifteen main coaches and over a 1000 member investors who are always happy to help new members.

Our dedicated team own hundreds of properties, including seven hotels and scores of HMOS and BTLs. Our Development & Conversions experts have £30m in their GDV pipeline. Our Commercial expert has transacted on over hundred commercial deals. There are no gurus, no BS but there is plenty of action.